Will Lower Mortgage Rates Unlock the Housing Market in 2025?

After two sluggish years of stagnant home sales, the big questions for 2025 are: Will mortgage rates finally follow the Fed’s cuts? And will they drop enough to revive demand and supply?

Jobs Growth Rebounds, But Unemployment Ticks Higher

The U.S. economy added 227,000 jobs in November, a strong rebound after October’s storm- and strike-driven slowdown. However, unemployment inched up from 4.1% to 4.2% [BLS].

Key Takeaway: October’s weak report (just 12,000 jobs) made a bounceback expected, but rising unemployment could signal economic cooling—a factor the bond market welcomed. If this trend continues, mortgage rates could soften as economic data aligns with the Federal Reserve’s goals.

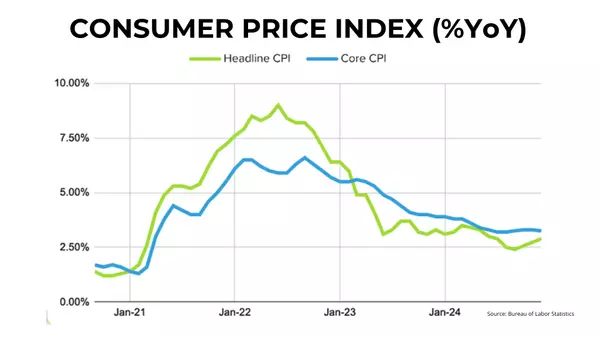

Inflation Stays Stubborn, Impacting Mortgage Rate Outlook

The November Consumer Price Index (CPI) report showed inflation remains sticky. Both “headline” and “core” CPI rose 0.3% month-over-month, pushing annual headline inflation to 2.7% YoY and keeping core inflation steady at 3.3% YoY [BEA].

Looking Ahead: We’ll see the November PCE report (the Fed’s preferred inflation measure) on December 20. October’s data already showed inflation creeping up—headline PCE rose to 2.3% YoY, and core PCE climbed to 2.8% YoY. If inflation remains elevated, it may delay significant mortgage rate relief in early 2025.

Rising Costs: Food Inflation Hits Consumers Hard

The latest Producer Price Index (PPI) showed prices rising 0.4% MoM in November, double the increase seen in October. Rising food costs, particularly chicken eggs, coffee, bacon, and orange juice, are putting additional strain on household budgets [BLS].

Home Purchase Sentiment Continues to Improve

Fannie Mae’s Home Purchase Sentiment Index rose for the fourth straight month, reaching 75.0 in November—the highest level since February 2022. This optimism is driven largely by consumer expectations that mortgage rates will decline [FNMA].

What This Means for Home Buyers: If rates do begin to ease, pent-up demand among buyers who’ve been sitting on the sidelines could re-enter the market.

Homeowner Equity at Record Levels

In Q3 2024, homeowner equity reached $17.5 trillion nationally, up 2.5% YoY, averaging about $300,000 per homeowner with a mortgage [CoreLogic].

The Wealth Effect: This increase gives homeowners significant equity to leverage for upgrades, moves, or tapping into their wealth for other investments. For sellers, this equity growth could encourage listings as confidence returns to the housing market.

Another Rate Cut Likely on December 18

The Fed Funds futures market is pricing in a 98% probability of a 25 basis point cut (0.25%) on December 18. If this happens, it will bring the total cuts during this cycle to 100 basis points (1.0%)—a positive sign for future mortgage rate relief.

2025 Outlook: Will Lower Mortgage Rates Finally Unblock the Market?

If inflation begins to cool and the Fed continues cutting rates, mortgage rates could trend downward in 2025. This shift would be a game-changer for buyers waiting for affordability to improve and for sellers hesitant to list due to higher borrowing costs.

The past two years of stagnant sales may give way to a much-needed boost in demand and inventory, especially as pent-up buyers and sellers re-enter the market.

Categories

Recent Posts

GET MORE INFORMATION