BLOGS

Everything we do is intended to make a difference in your life so that you can buy and/or sell with confidence.

VIDEOS

Check out our video resources to learn more about the buying and selling process

Advancing Multi-Family Housing: Legislative Updates and Market Insights

The housing market is buzzing with developments that could significantly impact multi-family properties in the Greater Boston area and beyond. As your trusted real estate expert at Digital Realty US, I keep a pulse on legislative updates and market trends to help you make informed decisions. Here ar

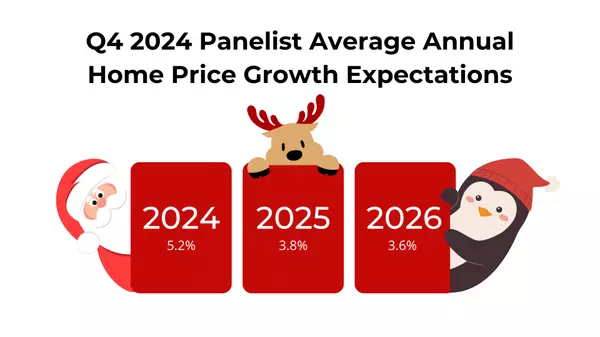

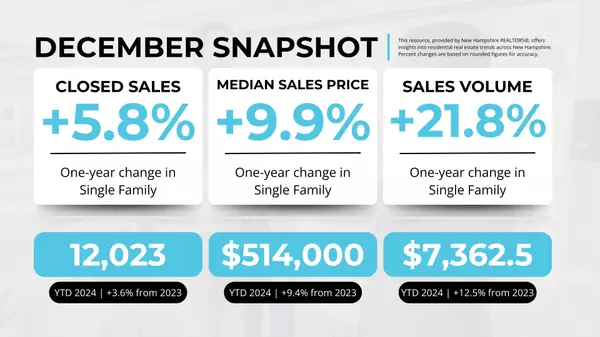

2024 in Review: NH Housing Market's Affordability Crisis

A historic year for New Hampshire's housing market ended with a median home price of $514,000, reflecting ongoing affordability challenges and limited inventory. The Tale of 2024: Affordability Hits Record Lows in New Hampshire The year-end median price of a single-family home in New Hampshire reach

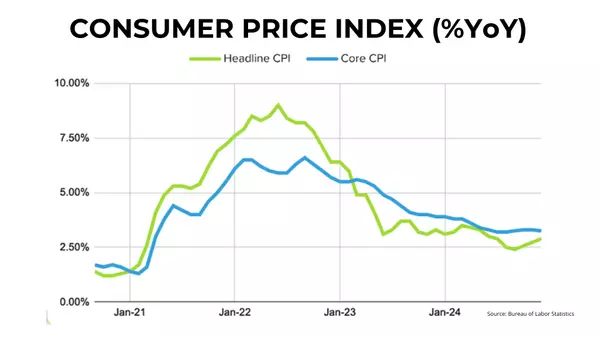

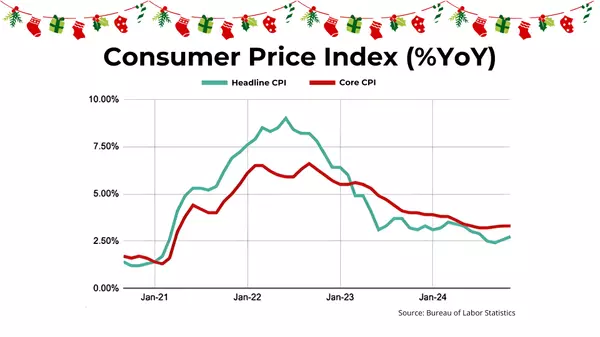

Mortgage Rates Stay High Amid Fed’s Conservative Rate Outlook

Despite cooling inflation, average 30-year mortgage rates remain above 7%, with the Fed unlikely to deliver a rate cut at its upcoming meetings. Here’s what Boston buyers need to know. Mortgage Rates Hold Steady Amid Fed’s Rate Strategy The December Producer Price Index (PPI) and Consumer Price Inde

Categories

Recent Posts