BLOGS

Everything we do is intended to make a difference in your life so that you can buy and/or sell with confidence.

VIDEOS

Check out our video resources to learn more about the buying and selling process

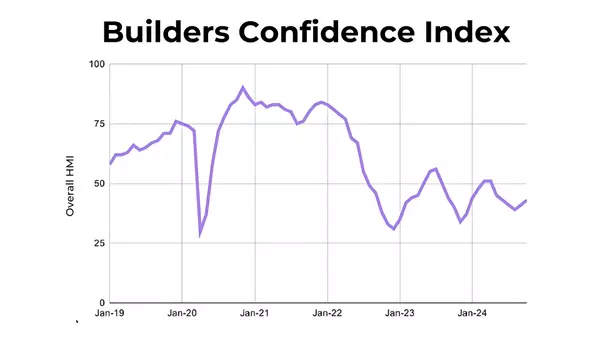

Builders Show Growing Confidence as Lower Mortgage Rates Drive Optimism

The National Association of Homebuilders (NAHB) Confidence Index saw an encouraging rise of 2 points in September, bringing it to 43. Now, while this number is still below the bullish threshold of 50 (which signals an expansionary environment for new home sales), it’s the second month in a row of im

Why Did Mortgage Rates Rise After the Fed Cut Interest Rates?

On September 18, the Federal Reserve surprised the market by cutting interest rates by 50 basis points, kicking off a new loosening cycle to ease financial conditions. Typically, when the Fed cuts rates, we expect borrowing costs, including mortgage rates, to decrease. However, in an unexpected turn

The MBTA Communities Act: A Path Toward Expanding Housing Near Transit in Massachusetts

By promoting multifamily housing near transit stations, the state is encouraging communities to take concrete steps to increase housing availability for residents across Massachusetts, including those in Greater Boston. What is the MBTA Communities Act? The MBTA Communities Act was introduced with t

Categories

Recent Posts