BLOGS

Everything we do is intended to make a difference in your life so that you can buy and/or sell with confidence.

VIDEOS

Check out our video resources to learn more about the buying and selling process

Boston's Proposed Business Tax Hike: What It Means for Local Businesses and Homeowners

Overview of Boston’s Commercial Property Tax Proposal Boston’s latest tax proposal, introduced by Mayor Michelle Wu, seeks to temporarily increase commercial property tax rates to alleviate a potential 27.8% rise in residential property taxes. This measure aims to protect homeowners from steep tax h

Metro Boston's Multifamily Housing Boom: Key Insights for Home Buyers and Investors

Introduction to Metro Boston’s Multifamily Surge As a seasoned real estate expert in the Massachusetts market, I’m excited to share critical insights on Metro Boston’s recent accolade as the fourth-ranked U.S. metro area for multifamily housing approvals. This recognition underscores the Greater Bos

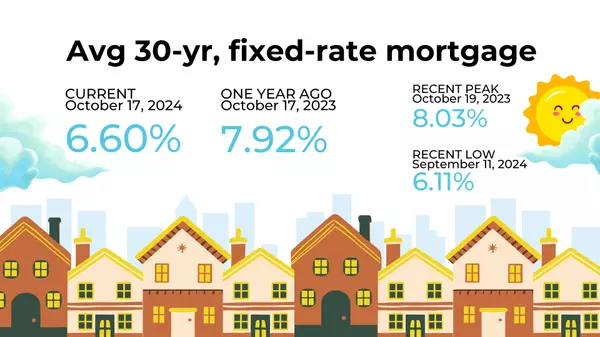

Mortgage Market Update: Steady Rates and Easing Inventory Bring Cautious Optimism

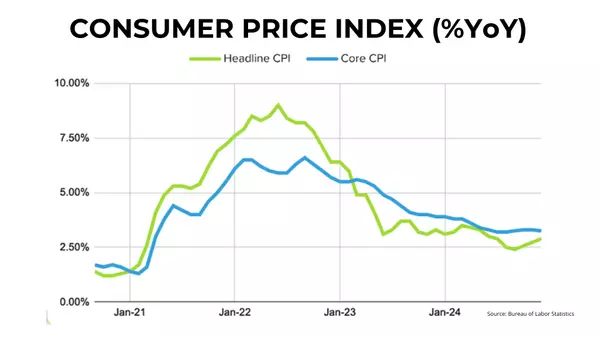

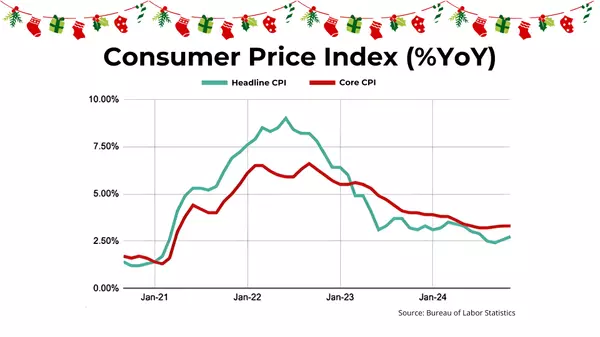

After last week’s uptick, average 30-year mortgage rates have held steady around 6.60%. It’s worth noting just how far we've come—in October 2023, mortgage rates peaked at a staggering 8.03%. Since then, rates have moderated significantly, a welcome change for today’s buyers. Current Fed Policy and

Categories

Recent Posts